If you’re an entrepreneur, understanding business credit vs personal credit isn’t just helpful—it’s essential. Many business owners unknowingly rely on their personal credit, putting their finances at risk and limiting their growth potential.

This guide breaks down the key differences between business and personal credit, why it matters, and how to leverage both to scale your business smarter.

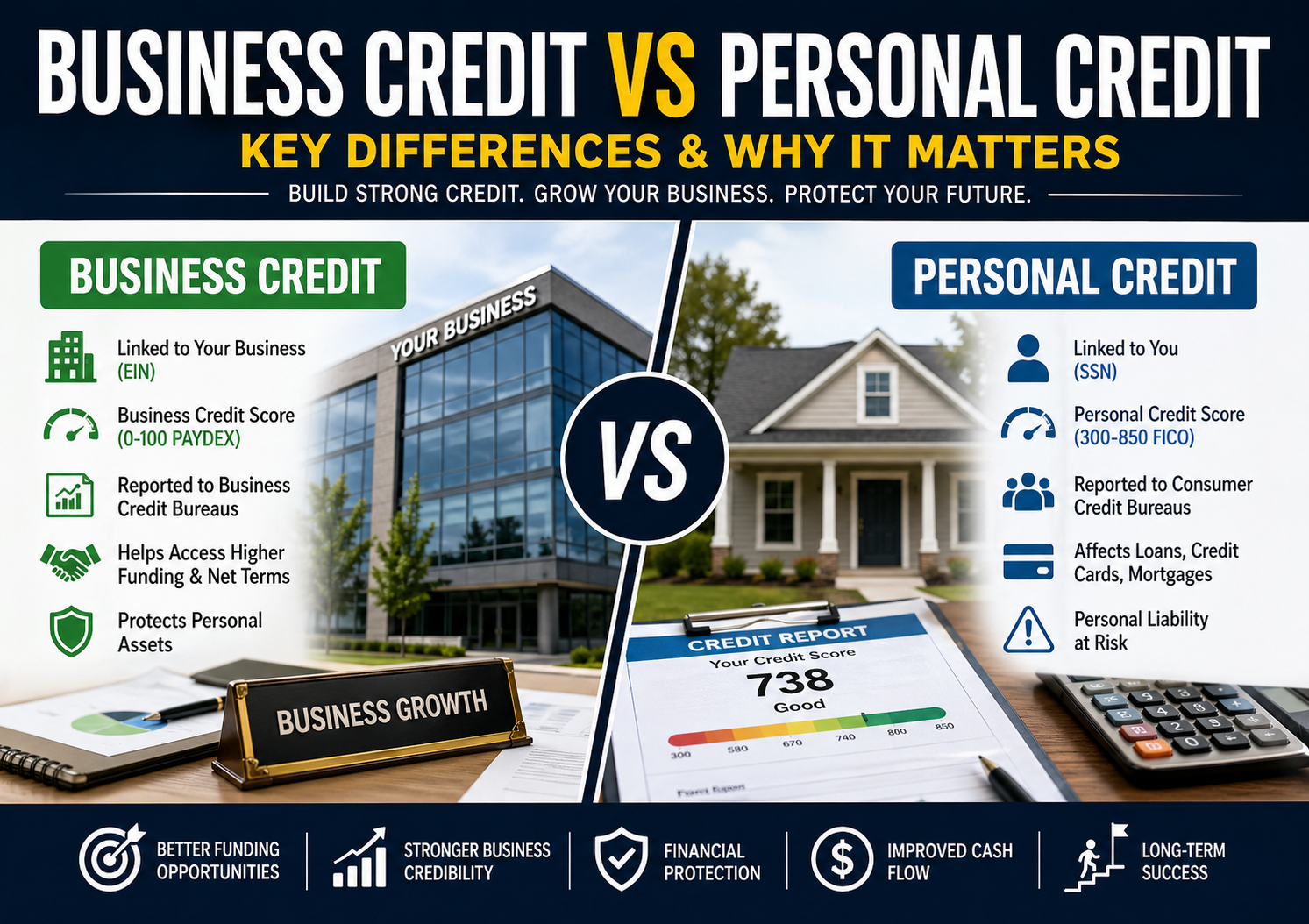

🔍 What Is Personal Credit?

Personal credit is tied directly to you as an individual. It reflects how you manage debt and financial obligations.

Key Features:

- Linked to your Social Security Number (SSN)

- Measured by scores like FICO (300–850)

- Includes credit cards, auto loans, mortgages, and personal loans

- Reported to major bureaus (Experian, Equifax, TransUnion)

👉 Lenders use this to evaluate your reliability as a borrower.

🏢 What Is Business Credit?

Business credit is separate from your personal finances and tied to your company.

Key Features:

- Linked to your EIN (Employer Identification Number)

- Tracked by business credit bureaus (Dun & Bradstreet, Experian Business, Equifax Business)

- Includes vendor accounts, business credit cards, and business loans

- Generates a business credit score (e.g., PAYDEX score)

👉 Strong business credit allows your company to stand on its own financially.

⚖️ Business Credit vs Personal Credit: Key Differences

| Feature | Personal Credit | Business Credit |

|---|---|---|

| Identifier | SSN | EIN |

| Credit Score Range | 300–850 | 0–100 (PAYDEX) |

| Liability | You personally | Your business |

| Reporting | Consumer bureaus | Commercial bureaus |

| Impact | Affects personal life | Affects business growth |

| Privacy | Public (some aspects) | Often more private |

💡 Why Separating Business and Personal Credit Matters

1. Protect Your Personal Assets

If your business fails and everything is tied to your personal credit, you’re personally liable. Business credit creates a financial barrier.

2. Access Higher Funding Limits

Business credit profiles can qualify for:

- Larger credit lines

- Higher loan approvals

- Better interest rates

3. Build Business Credibility

Vendors, lenders, and partners take you more seriously when your business has its own credit profile.

4. Improve Cash Flow

With business credit, you can:

- Get Net-30 / Net-60 terms

- Purchase inventory without upfront cash

- Manage expenses more efficiently

5. Avoid Personal Credit Damage

Using personal credit for business expenses can:

- Increase your utilization ratio

- Lower your score

- Limit personal financial opportunities

🚀 When Personal Credit Still Matters

Even with business credit, your personal credit may still be required:

- When applying for new business loans

- If your business is new or lacks credit history

- When signing a personal guarantee (PG)

👉 Strong personal credit helps you get started, while business credit helps you scale.

🛠️ How to Build Business Credit (Step-by-Step)

1. Register Your Business Properly

- Form an LLC or Corporation

- Get an EIN from the IRS

2. Open a Business Bank Account

Keep finances separate from day one.

3. Get a D-U-N-S Number

Register with Dun & Bradstreet to start your business credit file.

4. Establish Vendor Accounts

Start with vendors that report to credit bureaus:

- Net-30 accounts

- Office supplies, shipping vendors, etc.

5. Apply for a Business Credit Card

Use it responsibly and pay on time.

6. Monitor Your Business Credit

Track your reports and scores regularly to ensure accuracy.

⚠️ Common Mistakes to Avoid

- Mixing personal and business expenses

- Missing payments (even small ones)

- Applying for too much credit too fast

- Not checking your business credit reports

📈 Final Thoughts: Why This Matters More Than Ever in 2026

In today’s economy, access to funding can make or break a business. Entrepreneurs who understand business credit vs personal credit gain a major advantage.

Bottom line:

- Personal credit helps you start

- Business credit helps you scale

- Separating both protects your future