Unlocking Business Success with Insightful Funding Preparation

Securing business funding is a pivotal step for entrepreneurs and small business owners striving to grow their enterprises. Whether you’re seeking a loan, a line of credit, or alternative financing, understanding the approval process can significantly boost your chances of success. At Jdp Credit Solutions we empower clients with the knowledge and resources to navigate the sometimes perplexing landscape of business funding.

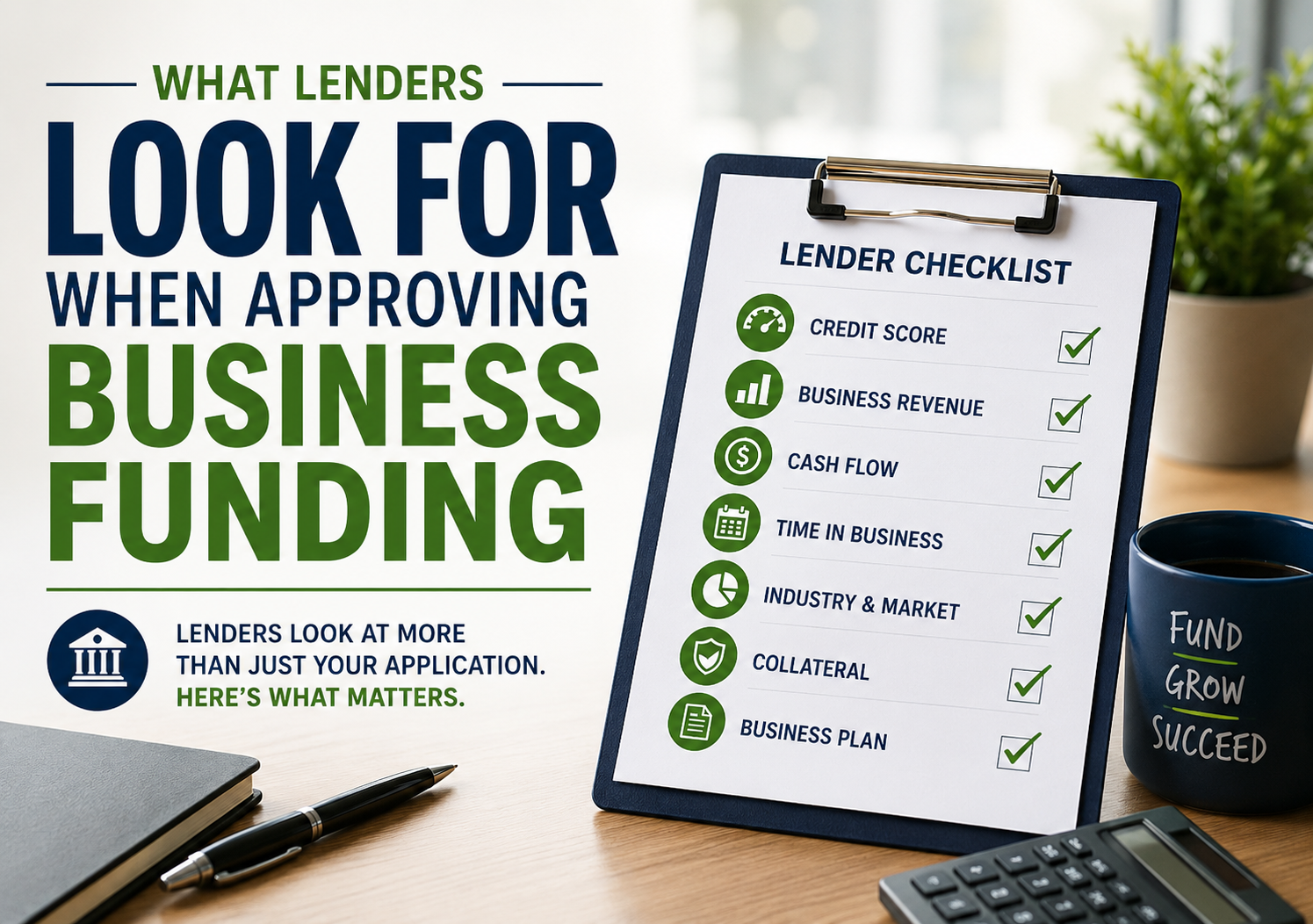

This comprehensive guide will delve into the key factors lenders evaluate when reviewing business funding applications. With this knowledge, you’ll be better prepared to present your business in the strongest light.

1. Your Business Credit Profile

Why It Matters:

Much like personal credit, your business credit profile signals your company’s reliability and track record in managing debts. Lenders rely on this information to assess your trustworthiness.

What Lenders Look For:

- Credit Score: Most lenders prefer to see a business credit score above 75 on the PAYDEX score or a FICO Small Business Scoring Service (SBSS) score above 140.

- Credit History: A history of late payments, defaults, or bankruptcies can be red flags.

- Existing Debt: High existing debt in relation to your available credit can hurt your chances.

How to Improve:

- Pay bills on time

- Check your business credit report regularly for errors and disputes

- Build relationships with vendors that report payments to credit bureaus

Check out our credit repair services to learn how we can help strengthen your business credit profile.

2. Personal Creditworthiness

Why It Matters:

If your business is relatively new or lacks substantial history, lenders will scrutinize your personal credit. This is especially common with sole proprietors or closely held small businesses.

Key Aspects:

- Personal Credit Score: Lenders often look for a FICO score of 680 or higher

- Credit Utilization: Lenders want to see that you use credit responsibly

- Debt-to-Income Ratio: Excessive personal debt may limit your approval odds

Tips:

- Monitor your personal credit report regularly

- Correct any errors immediately

- Reduce outstanding personal debt where possible

3. Business History and Financial Health

Why It Matters:

Lenders prefer businesses that have a proven track record. Your business’s longevity and financial statements provide insight into its stability.

What Lenders Look For:

- Time in Business: Many lenders require at least 1-2 years of operational history

- Annual Revenue: Higher, consistent revenues mean lower risk for lenders

- Profit Margins: Profitability indicates your ability to repay debt

- Tax Returns: These verify your reported income and provide transparency

How to Prepare:

- Have up-to-date financial records ready (balance sheets, profit & loss statements)

- Keep personal and business finances strictly separate

- Consult with a financial advisor if necessary

4. Collateral and Equity Investment

Why It Matters:

For some funding types, especially secured loans, lenders require collateral to mitigate risk. They may also look for owner’s equity investment as a sign of commitment.

Typical Collateral Can Include:

- Real estate

- Equipment or inventory

- Accounts receivable

- Personal assets (as a last resort)

Equity: Lenders want to see you have invested your own money into the business. This demonstrates your confidence and willingness to take risks alongside them.

Tip:

- Be ready to provide a detailed list of assets and proof of ownership

5. The Business Plan and Loan Purpose

Why It Matters:

A well-defined business plan assures lenders that you’ve thoroughly considered your market, growth strategy, and potential risks.

Key Elements Lenders Want:

- Executive Summary: Clear and concise overview

- Financial Projections: Realistic estimates of income and expenses

- Loan Purpose: A specific and justified use of funds (e.g., equipment purchase, inventory, expansion)

- Market Analysis: Understanding of competitors and customer base

Pro Tip: Even if you’re not asked for a business plan, having one ready can set you apart.

6. Cash Flow Analysis

Why It Matters:

Ultimately, lenders want to ensure you can generate enough cash to repay the loan. Cash flow statements show how money moves in and out of your business.

Lenders Evaluate:

- Operating Cash Flow: Are revenues sufficient to cover expenses and debt payments?

- Cash Flow Projections: Forward-looking estimates provide insight into future repayment capacity

- Liquidity Ratios: Such as current ratio and quick ratio

How to Improve:

- Address late-paying customers

- Cut unnecessary expenses

- Monitor and manage accounts payable and receivable closely

7. Industry Risks and Market Conditions

Why It Matters:

Lenders prefer stable industries with predictable revenue streams. Highly cyclical or declining sectors may face additional scrutiny or stricter terms.

Assessment Factors:

- Industry Trends: Is your sector growing, declining, or volatile?

- Regulatory Changes: Are there new rules that could affect your profitability?

- Seasonality: Sharp fluctuations can present repaying challenges

Action Item:

- Be prepared to explain how you mitigate industry-specific risks

Conclusion: Get Ready With Jdp Credit Solutions

The business funding landscape can be challenging, but you don’t have to navigate it alone. At Jdp Credit Solutions, we help individuals and small businesses in Miami and beyond improve their credit, prepare their funding applications, and unlock the financial resources they need to thrive. By understanding what lenders look for and proactively addressing these areas, you’ll dramatically increase your chances of obtaining the business funding your company needs for success.

Ready to take the next step? Contact us today for expert support and personalized funding solutions!

Empowering your financial future, one step at a time.