Debt consolidation can be a powerful financial tool for regaining control of your money. By rolling multiple debts into one manageable loan, you can simplify payments, reduce interest rates, and potentially pay off debt faster. However, before you jump into applying, there are key steps you should take to ensure this option works in your favor.

In this guide, we’ll walk you through the essential steps to take before applying for a debt consolidation loan so you can make smart financial decisions and improve your chances of approval.

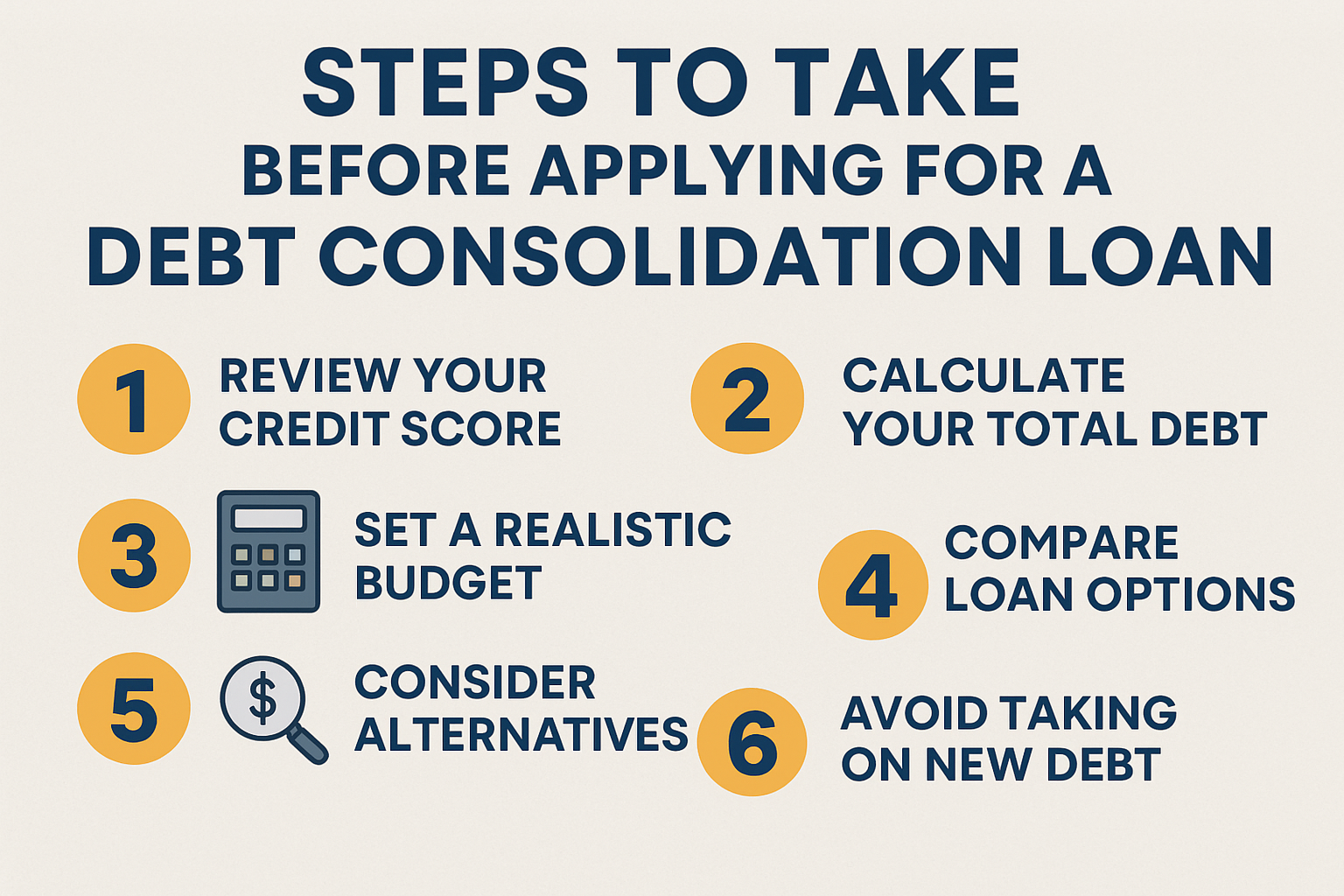

1. Review Your Credit Score

Your credit score plays a major role in whether you qualify for a debt consolidation loan and the interest rate you’ll receive. Lenders prefer borrowers with good to excellent credit because it signals lower risk.

🔹 Action Step: Pull your free credit report from all three bureaus (Experian, Equifax, TransUnion) at AnnualCreditReport.com. Review for errors and dispute any inaccuracies that may be lowering your score.

2. Calculate Your Total Debt

Before consolidating, you need a clear picture of your financial situation. Knowing your exact debt total helps you determine whether consolidation will actually save you money.

🔹 Action Step: Make a list of all your debts, including credit cards, personal loans, and other balances. Record the interest rate, monthly payment, and remaining balance for each.

3. Set a Realistic Budget

Debt consolidation won’t work unless you can consistently make payments on your new loan. Creating a budget allows you to see how much room you have for a consolidated payment.

🔹 Action Step: Track your monthly income and expenses. Identify areas where you can cut spending to free up money for debt repayment.

4. Compare Loan Options

Not all debt consolidation loans are the same. Banks, credit unions, and online lenders each offer different terms, interest rates, and fees. Shopping around ensures you get the best deal.

🔹 Action Step: Request prequalification quotes from multiple lenders to compare interest rates and terms without impacting your credit score.

5. Consider Alternatives

A loan may not always be the best option. Depending on your situation, alternatives like a balance transfer credit card, negotiating with creditors, or enrolling in a debt management plan may be more effective.

🔹 Action Step: Explore all options before committing to a loan. Choose the strategy that minimizes costs and aligns with your financial goals.

6. Avoid Taking on New Debt

Consolidation only works if you commit to breaking the debt cycle. Taking on new debt while paying off your consolidation loan defeats the purpose and can leave you worse off.

🔹 Action Step: Stop using credit cards for non-essential purchases and focus on sticking to your repayment plan.

Final Thoughts

Applying for a debt consolidation loan can be a smart way to simplify your finances and work toward becoming debt-free. But the key to success lies in preparation. By reviewing your credit, calculating your debt, creating a budget, and exploring all options, you’ll put yourself in the best position to secure favorable terms and avoid future financial stress.

✅ Pro Tip: Lenders want to see responsible financial behavior. Start improving your credit today, and you’ll increase your chances of getting approved for a debt consolidation loan with a lower interest rate.